Edge CSB Bank Credit Card MITC

These Most Important Terms and Conditions (“MITC”) apply to the Edge-CSB Bank Credit Card issued by CSB Bank Limited (Bank) in partnership with its co-branding partner Europa Neo Marketing Private Limited (formerly known as Amica Neo Marketing Private Limited) (“ENMPL”).

Cardholders can activate the Edge CSB Bank Credit Card exclusively on the Jupiter Mobile App (owned by Amica Financial Technologies Private Limited (“Jupiter”) or clicking on ‘Submit’ or ‘I Agree’ or any similar tab/icon would mean acceptance of the MITC by the cardholder/Cardholder/user/you (“Cardholder”).

The MITCs are in addition to and are to be read along with the detailed Terms and Conditions and are subject to change at the discretion of the Bank and in accordance with laws as applicable from time to time. An updated version will always be available on the Bank’s web page and in the Jupiter App.

Schedule of Fees and Charges

The following charges are at the sole discretion of the Bank and can be changed at any time after giving one month’s notice.

Here is a list of all charges (exclusive of all applicable GST):

*Joining and Annual Membership fee for the primary user is Nil only for the first two lakh customers. Such fee shall be notified at the time of availing the credit card on the Jupiter App

** Overlimit - While we do not generally allow overlimit transactions. In case Cardholder’s credit limit is breached due to a higher amount presented by the merchant at the time of settlement, there will be no charges levied.

*** Users to be eligible for Fuel Surcharge Waiver of Rs. 100 per billing cycle

TDS wherever applicable shall be deducted for the customer as per the rates notified by the government from time to time.

Late Payment Charge

Late payment charge will be applicable if the Minimum Amount Due (“MAD”) is not paid by the payment due date.

Illustrative example for calculation of Late Payment Charge:

In the example below, consider the billing cycle is 1st of the calendar month - end of the month. Statements are generated on the 1st and are due on the 15th of every month. There is no outstanding at the start of the following cycle.

Note: Late Payment Charge is not applicable when the total outstanding is less than ₹500.

Interest Charges

- Interest will be charged if the Total Amount Due (“TAD”) is not paid by the payment due date. Interest will be charged on the outstanding amount due and on all new transactions (from the transaction date) till such time as the total amount due is paid in full.

- The following example shows how interest is calculated. In the table given below, it has been assumed that the Total Amount Due (“TAD”) of the previous month’s statement has been paid by the payment due date and there is no outstanding amount. The statement generation date is the 1st. Given these assumptions, interest will be calculated as shown:

4. On statement dated 1 May 2024, the following interest charges will be levied. Interest is calculated using the following formula:

Note: These illustrations are meant to be indicative and to show how interest is calculated and charged.

Interest Free Period

The interest free period could range from 13 to 47 days.

Example for the calculation of interest free period:

For a statement for the period from May 1, 2024 to May 31, 2024 the payment due date would be Jun 15, 2024. Assuming that the cardholder has paid the Total Amount Due of the previous month statement by the payment due date, the grace period would be:

- For a purchase dated May 2, 2024, the interest-free grace period is from May 2, 2024 to June 15, 2024, i.e. 45 days.

- For a purchase dated May 30, 2024, the interest-free grace period is from May 30, 2024 to June 15, 2024, i.e. 17 days.

Thus, the grace period can vary depending upon the date of purchase. Note:

If the Total Amount Due is not paid by the payment due date, then there will be no interest free period.

For cash advances, interest is charged from the date of the transaction until the date of payment.

There is an additional three day period (as mandated by the Reserve Bank India “RBI”) post the payment due date during which if the Cardholder makes a payment, they will not be charged late payment or interest charges

Forex Markup Fee

If a transaction is made in a currency other than Indian Rupees, that transaction will be converted into Indian Rupees.

The conversion will take place on the date the transaction is settled which may not be the same date on which the transaction was made.

If the transaction is not in USD (US Dollars), the amount will first be converted to USD, and then the USD amount will be converted to INR as per the rate provided by international network partners of RuPay . On this amount, a forex markup fee will be levied, and GST will be applicable on the markup fee.

If this transaction is reversed, both the markup fee and GST charges will be refunded. In case of a refund, however, only the transaction amount will be refunded in INR as per the conversion rate applicable on the date of refund.

A forex markup fee will also be levied in case of an Indian Rupee (INR) transaction done at a merchant or payment gateway that is based out of India.

Credit Limit

Cardholder’s Credit Limit will be communicated to them at the time of card issuance. This will also be mentioned in the monthly statements.

Available credit limit is calculated by deducting the utilised limit from the Total Credit Limit. “Available Credit Limit” is the limit up to which a cardholder can make purchases.

Cardholders may be entitled to apply for an enhancement of the Credit Limit after 12 months from the date of card issuance. CSB Bank also reserves the right to recommend a Credit Limit increase to the Cardholders based on their Edge CSB Bank Credit Card usage, in the Jupiter app. This recommendation and its associated terms and conditions will be made available for the Cardholder to consider before accepting the recommendation.

Once the Cardholder has read and agrees to the Terms related to Credit Limit increase displayed inside the Jupiter app and provided their consent to increase the limit, their Credit Limit will be enhanced. Cardholder’s acceptance of the limit increase recommendation where they specifically validate the limit increase and agree to the terms will be treated as a consent. The Bank or its authorised third party service provider, will keep the digital records of such consent and will treat it as proof of consent in case of any dispute arising later on account of limit increase.

CSB Bank will review the Cardholder’s account periodically and reserve the right to decrease their credit limit based on their transaction patterns, payment behaviour and other internal criteria. This will be informed to the Cardholder via the Jupiter app and/or via email and SMS.

Billing

1. Payment Schedule

The billing cycles have been illustrated based on examples below-

2. Billing statements

The Cardholder’s billing statement will be generated every month. It will contain a break-up of all purchases, payments, fees, interest charges, refunds and taxes.

In case the card was not used in a month, the statement will mention there were no spends in that month. Jupiter App also has an option to view and download the statement in PDF format. The Cardholder will also be sent a PDF copy of their monthly statement on their registered email address. The Cardholder shall, however, review the statement from time to time on Jupiter app in order to stay updated on the statement.

Only settled transactions will be included in the monthly statement. In case a transaction done in a particular cycle has not been settled by the time of statement generation, it will be included in the next cycle. As per the Network Partner guidelines, merchants are given up to a maximum of 10 days to settle domestic transactions and 15 days to settle international transactions.

In case a transaction is not settled in this timeframe, the transaction amount will be refunded to the Cardholder. After this, in case of late presentment of the transaction for up to 45 days from date of transaction, they can be charged again and their available limit reduced accordingly.

Any transactions on which a dispute has been raised, will not be included in the monthly statement.

3. Minimum Amount Due

The Cardholder will need to pay at least the Minimum Amount Due by the Payment Due Date as indicated in the monthly statement. If they have paid the Minimum Amount Due, they will be liable to pay interest only on the outstanding amount and can continue to earn and redeem rewards.

Minimum Amount Due stated in the monthly statement shall be calculated as per the following formula:

If the minimum amount due is less than ₹500, the Cardholder will be charged ₹500 as the minimum amount due. If the total amount due is less than ₹500 then the total amount due value becomes the minimum amount due.

4. Payment knock-off order:

When the Cardholder makes a payment, it is adjusted in this order:

- Taxes

- Fees

- Interest

- Purchases

Furthermore, purchase amounts are knocked off starting with the earliest transaction date.

5. How Refunds/Reversals/Waivers/Chargebacks impact the statement

The Cardholder must pay for the transactions billed in the Edge CSB Bank Credit Card statement to avoid any additional charges being levied. However, if they receive any incoming transactions (refunds, reversals, waivers or chargebacks) before having cleared the bill, these transactions will first offset the total amount due on the last statement.

If there is no billed amount due, this amount will be adjusted against their current outstanding. If there are no outstanding dues on the card, we will adjust incoming transactions only up to ₹5000 or 1% of the Cardholder’s Credit Limit (whichever is lower), and any excess balance will be refunded to their specified bank account.

6. Method of payment

The Cardholder can pay the outstanding dues from the Jupiter app using the following modes:

- Auto-debit from their bank account on Jupiter App. This auto-debit will be initiated at 10 AM on the payment due date

- Bank transfer from their bank account on Jupiter App or other Registered Bank Account.

- UPI payments (up to ₹2 lakh) from any Bank Account added to the Jupiter UPI App.

- Via debit card and netbanking of any bank account using a unique payment link sent to the Cardholder via SMS and email.

CSB Bank has the right to add/remove any methods of payment at any time.

7. Billing disputes resolution

All the contents of the statement will be deemed to be correct and accepted if the Cardholder does not inform us of any discrepancies within 30 days of the statement generation date. In the event of billing disputes/discrepancies, we shall investigate and confirm the liability for such transactions.

For any disputes which result in a chargeback being raised, we may offer a temporary credit during the period of investigation, which may be reversed along with applicable charges subject to outcome of the investigation.

Any GST levied will not be reversed in any dispute on fees and charges or interest.

8. Contacting us in case of a billing dispute

In case the Cardholder needs any help, they can:

- Click on the (?) button on the Jupiter app and use the chat support to get a resolution

- Call our Customer Care number at +91 86550-55086

- Email us at edge-csb-support@jupiter.money

- Writing to Smt M Sreelatha, Principal Nodal Officer for Customer Grievances, CSB Bank Limited, Head Office, CSB Bhavan, St Mary’s College Road, Thrissur – 680020 Kerala.

- Tel: 0487-2333020. In all communications with us, please indicate the complete registered mobile number and the last 6 digits of your Edge CSB Bank Credit Card number.

Refund of credit balance/excess amount

In case there is a credit balance/excess amount lying in the Cardholder’s Edge CSB Bank Credit Card account due to an additional payment or a reversal/refund, this amount will be refunded (without any applicable interest) to them as long as all their outstanding dues are cleared.

The following procedure will be followed:

- If the Cardholder has a partner bank account on the Jupiter app, the excess credit balance will be automatically transferred to that account

- If the Cardholder has opted for the Edge CSB Bank Credit Card but doesn't have a partner bank account on the Jupiter platform, they’ll need to enter their bank account details on the Jupiter app. This account must be active and the Cardholder must be the primary account holder. We will deposit Re. 1 into that account to verify the bank account details.

Few things to remember:

- In case the Cardholder has no outstanding dues and if they received an incoming transaction of greater than ₹5000 or 1% of their Credit Limit (whichever is lower), this amount will be transferred to their respective account within 3 working days. This is applicable for both active and blocked cards.

- If the Cardholder does have any outstanding dues, any refunds, reversals, waivers or chargebacks will be adjusted in the manner stipulated under clause a. This is applicable for both active and blocked cards.

- If the Cardholder’s Edge CSB Bank Credit Card account has been closed, they can still provide their bank account details on the Jupiter App. Any excess balance or credit amount will be transferred to that bank account within 7-10 working days from the date of such request. If they have an existing partner bank account on the Jupiter app, this amount will be transferred directly to that account in the same timeframe. In case there is no access to the Jupiter app, they can share a cancelled cheque or provide their bank account details by emailing us at support@jupiter.money.

- In case of an active card or blocked card, any excess credit resulting from excess payment will be reversed if a request for the same is placed with Jupiter. This reversal will be done within 7 working days from the date of such request into the respective bank account.

- No interest will be payable on any credit balance/excess amount lying in the Cardholder’s Edge CSB Bank Credit Card account.

Rewards and Benefits

By using the Edge CSB Bank Credit Card, you get access to certain rewards and benefits.

Earning rewards

- Upto 5% Cashback on UPI-Credit Card Spends:

- This offer is applicable to UPI Edge CSB Bank Credit Card transactions made through any UPI app for transactions pertaining to UPI Intent, UPI-Scan & Pay, and UPI-Collect requests.

- Cashback rates may vary and will be subject to the terms communicated by the Bank or partner.

- Eligibility for cashback is subject to MCCs determined by the bank.

- Spend Rs. 1000 and earn 250 Jewels.

- For Every 5 Jewels can be redeemed either for Gold equivalent of Rs. 1 or Gift Voucher (if applicable). Start earning on a minimum spend of Rs. 100.

2. Accelerated Cashback for Bill Payments & Gift Voucher Purchase on Jupiter App:

- Accelerated cashback is applicable to bill payments and voucher purchases made through the Jupiter App.

- The specific cashback rates will be notified by the bank/partner through the Jupiter App.

3. Flat 1% Cashback on Rupay Credit Card Spends:

- This offer provides a flat 1% cashback on all Edge CSB Bank Credit Card transactions, including online and in-store purchases.

- Spend Rs. 1000 and earn 50 Jewels. 5 Jewels can be redeemed either for Gold equivalent of Rs. 1 or Gift Voucher (if applicable). Start earning on a minimum spend of Rs. 100.

4. Welcome Voucher of Rs. 250/- on 1st Successful Transaction with Partner Brands:

- A welcome voucher will be issued to customer valued at Rs. 250/- after the first successful UPI Credit card transaction from the Edge CSB Bank Credit Card on Jupiter App. User can select any one voucher via partner brands such as Amazon, Flipkart, Swiggy, Zomato, or Myntra.

- The voucher will be available on the Jupiter app and sent to the Cardholder's registered communication channel as per the records.

5. Lounge Benefit:

The Cardholder is entitled to complimentary lounge access at domestic airport lounges as specified below:

- Domestic: 1 lounge visit per calendar quarter, totalling up to 4 lounge visits per calendar year. (₹2+GST will be charged to the Credit Card for the lounge access).

- Spend milestone to unlock lounge access for the user shall be Rs. 50,000 spent within any given 3 consecutive months

- Any incremental will be charged on actuals at the lounge itself

- If the milestone is not achieved and the user visits the lounge, the visit will be enabled but at a charged rate of Rs. 1700 per lounge visit.

- No international lounge access would be enabled

- User will be notified of their eligibility once swiped at lounge itself

- Complementary Lounge Access:

- Cardholders are entitled to one lounge visit per calendar quarter, totalling up to four lounge visits per calendar year.

- A charge of ₹2 plus GST will be levied on the Credit Card for each lounge access.

2. Spend Milestone for Lounge Access:

- To qualify for complimentary lounge access, the Cardholder must meet a spending milestone of Rs. 50,000 within any given three consecutive months.

3. Charges for Exceeding the Complementary Lounge Access:

- Any incremental charges for lounge access beyond the entitlement will be assessed based on actual costs incurred at the lounge.

- If the spending milestone is not met, and the Cardholder still chooses to access the lounge, each visit will incur a charge of Rs. 1700.

- Exclusively Domestic Lounge Access:

- Please note that this lounge access program is restricted to domestic lounges, and no access will be provided for international lounges.

- Eligibility Notification:

- Users will receive notifications confirming their eligibility once they swipe their card at the lounge.

6. Insurance and Concierge Service:

This benefit is limited to Platinum Variant Card.

Redeeming Rewards and Benefits

1. Jupiter offers rewards in form of Jewels only on the Jupiter app

2. Jewels are redeemable as cash on the Jupiter App, min. of 100 Jewels need to be accumulated prior to redemption.

3. Jewels are also redeemable as digital gold, subject to users acceptance of terms and conditions.

4. Jupiter may introduce new redemption opportunities for users in the future, the T&Cs of which will be updated prominently to the user.

5. Earning and Redemption of Jewels earned for Edge CSB Bank Credit Card is dependent on the payment of the Minimum Amount Due for your latest bill. If the minimum amount due is not paid, any Jewels earned in the cycle will be locked for redemption. Moreover, earning of Jewels will be paused till the time the minimum amount due is paid in full.

6. 5 Jewels = Rupee 1/-, this is subject to change by giving 1 month prior notice to the customer.

Other Terms:

1. Jewels which have been credited or debited to or from your Edge CSB Bank Credit Card account shall be reflected on the Jupiter app. You can also view the Jewels accumulated by you on the Jupiter app.

2. AFTPL as authorised by the Bank reserves the right to wholly or partly modify the Edge CSB Bank Credit Card Rewards Programme. The reward points, conversion rate, and withdrawal of Jewels awarded may be modified from time to time.

3. In case the Edge CSB Bank Credit Card Rewards Programme comes in conflict with any rule, regulation or order or any statutory authority, then the rewards programme may be modified or cancelled to give effect to said requirements.

4. Jewels do not expire and have lifetime validity, except in circumstances detailed below:

- If the Edge CSB Bank Credit Card is not used for more than 365 days, the accrued Jewels will be nullified.

- If the user doesn’t pay their outstanding dues for 90 days, all Jewels accrued will lapse.

5. AFTPL as authorised by Bank reserves the right to cancel or suspend the accrued Jewels if the Edge CSB Bank Credit Card account is in arrears, suspension or default or if the Edge- CSB Bank Credit Card account is or is reasonably suspected to be operated fraudulently.

6. In case of Cardholder’s death, the Jewels earned but not redeemed at that time will be forfeited.

7. If a transaction is reversed by way of a refund/chargeback/reimbursement, the transaction amount shall be credited back to your Edge- CSB Bank Credit Card account. In such instances, the Jewels accrued on those transactions will be reduced from the overall Jewels balance.

8. On closure/termination of Edge CSB Bank Cardholdership, any Jewels pending to be claimed in the Cardholder’s account will be forfeited.

9. AFTPL as authorised by the Bank will not be held responsible if any supplier of products / services offered to you withdraws, cancels, alters or amends those products/services.

10. AFTPL as authorised by the Bank makes no warranties for the quality of products / services provided by the merchant establishments participating in the Jupiter Edge- CSB Bank Rewards Programme.

11. Jewels are not awarded for certain merchant categories (classified as MCC by Network Partners). This list can be seen in the “Terms and conditions”.

12. The Bank/AFTPL can block earning of Jewels on any merchant if there is a reasonable suspicion of fraud.

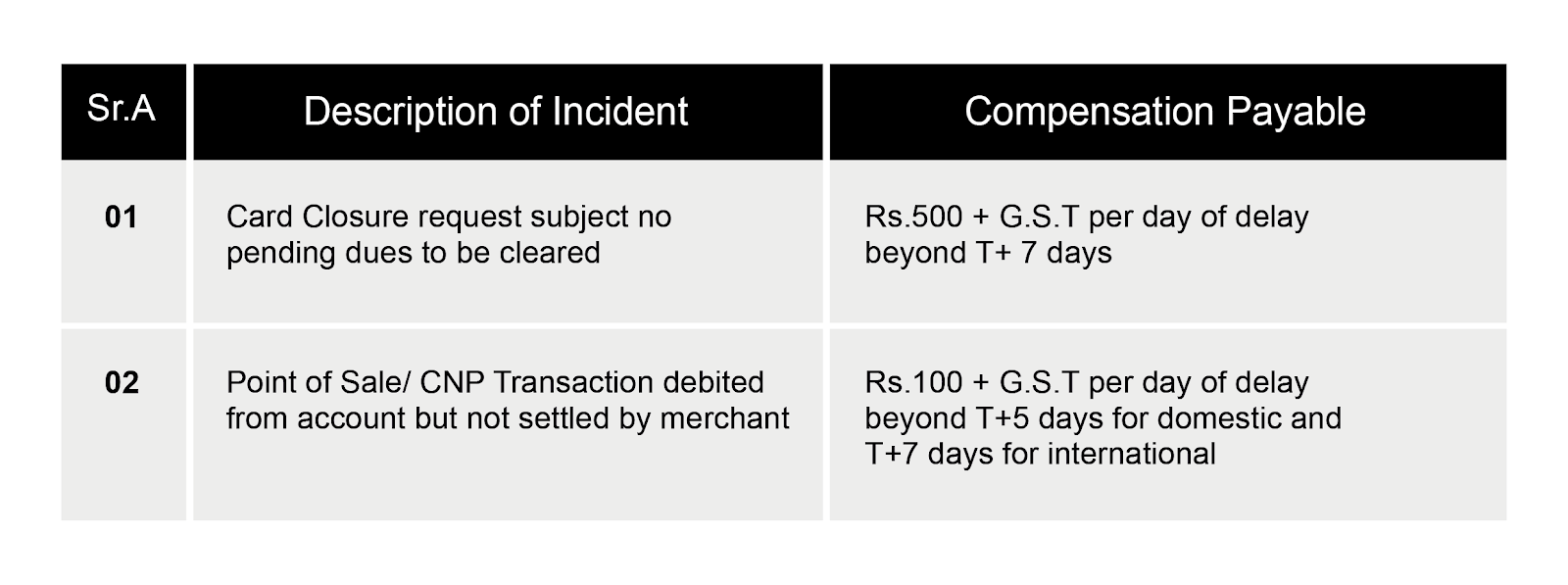

Grievance Redressal and Compensation Framework

i) In the event that you are not satisfied with our services, you may register your grievance by

- Calling us at our CustomerCare number at +91 86550 55086

- Emailing us at grievance@jupiter.money

- Beyond this level, you can reach out to the bank on edge-csb-support@jupiter.money if you do not get a satisfactory response to your comfort.

- If you are not satisfied with the above, you may escalate the matter to Smt M Sreelatha, Principal Nodal Officer for Customer Grievances, CSB Bank Limited, Head Office, CSB Bhavan, St Mary’s College Road, Thrissur – 680020 Kerala.

Tel: 0487-2333020. In all your communications with us, please indicate your complete registered mobile number and Edge CSB Bank Credit Card number.

If the issue remains unresolved beyond 30 days even after reaching out to the above channels, or if the response is unsatisfactory, you may write to the Banking Ombudsman for an independent review. Details of the Banking Ombudsman Scheme are available on the RBI website at https://www.rbi.org.in/.

ii) Below compensation framework will be followed in case of delay in resolving

iii) Contact details of the card-issuer are as follows:

Email your query to customercare@csb.co.in

Call on helpline number at 1800-266-9090

Default and Circumstances

In the event the Cardholder fails to make the payment of Minimum Amount Due by the due date, interest shall be levied as per the rates mentioned above and the Cardholder shall not be entitled to redeem any Jewels and further earnings of the Jewels shall be stopped from the date of end of the three-day grace period.

Procedure including notice period for reporting a Cardholder as defaulter

In the event of default, the Cardholder will be sent reminders from time to time for settlement of any outstanding amount on the Credit Card account using any of the following modes: by post, telephone, e-mail, SMS messaging and/or engaging third parties to remind, follow up and collect dues. Any third party so appointed, shall adhere fully to the Code of Conduct on debt collection as applicable from time to time. Occurrence of one or more of the following events shall constitute an event of default and CSB Bank at its sole discretion may withdraw the Credit Card facility:

- The Cardholder fails to pay any amount due to the Bank within the stipulated period of 180 days;

- The Cardholder fails to perform the obligations as per Cardholder Terms;

Any NACH/standing instructions are not encashed/acted upon for any reason whatsoever on presentation/being made - Any representation made by the Cardholder proves to be incorrect, false, or incomplete, including but not limited to income and/or identification papers/documents forwarded to the Bank being proved incorrect, incomplete, and or containing false fraudulent information

Procedure for withdrawal of default report and the period within which the default report would be withdrawn after settlement of dues:

- The defaulter in question has liquidated his entire outstanding dues with the Bank or settled his dues with the Bank.

- A court verdict has been received against the Bank,in a legal suit filed by or against the Bank, instructing the Bank to de-list the Cardholder from the default report. Decisions are taken on a case to case basis upon individual reviews.

Recovery procedure in case of default

In case of default, the Bank can recover the amount by referring the dispute to a sole arbitrator, appointed by a designated officer of the Bank under the provisions of the Arbitration and Conciliation Act, 1996 as amended from time to time. The seat of arbitration shall be Mumbai, India. The arbitration proceedings shall be in English Language

Termination/Revocation/Surrender of Card membership

Procedure for surrender of card by Cardholder

- The Cardholder can close their Edge CSB Bank Credit Card account any time from the Jupiter app by navigating to the Edge CSB Bank Credit Card settings or by calling, emailing or initiating a chat with the customer support team. The entire card outstanding dues and loans / EMI facilities linked to their Edge CSB Bank Credit Card (if applicable and/or availed of) will have to be cleared before submitting the card closure request.

- Any refund/reversal that is received after the card closure will be intimated to the Cardholder and refunded electronically to the respective account i.e. the partner bank account opened on Jupiter App or any other account specified by the Cardholder on the Jupiter App.

- Upon termination/revocation of Edge CSB Bank Credit Card holdership for any reason whatsoever, whether at the instance of the Cardholder or the Bank, the Cardholder shall remain liable for all charges incurred using the Edge CSB Bank Credit Card.

- The Cardholder specifically acknowledges that once their Edge CSB Bank Credit Card account is closed, the privileges (including but not limited to all benefits and services accrued, Jewels not redeemed etc) of the Edge CSB Bank Credit Card stand nullified. Reinstatement of the same is neither automatic nor attendant and will take place solely at the discretion of the Bank.

- For avoiding misuse, it is advised to destroy the Edge CSB Bank Credit Card ensuring that the hologram, magnetic strip and chip are destroyed permanently.

- The Cardholder’s Edge CSB Bank Credit Card account will be closed only if the Bank receives the payment of all amounts due and outstanding in respect of the said Edge CSB Bank Credit Card account.

Procedure for revocation of Cardholdership

The Cardholder’s access to their Edge CSB Bank Credit Card may be cancelled or revoked at any time without prior notice, if we consider it necessary for business or security reasons, which may include but are not limited to:

- Delayed or dishonoured payments, improper use of credit card (in violation of RBI and Foreign Exchange rules).

- Misleading or incorrect information / documents given along with card application.

- Failure to furnish information or documents as required under the Know Your Customer (KYC)/ Anti Money Laundering (AML)/ Combating the Financing of Terrorism (CFT) guidelines.

- Involvement in any civil litigation or criminal offence / proceedings by any authority, court of law or professional body or association.

- Changes in credit policy due to prevailing conditions / unforeseen circumstances. The Cardholder may continue to get their Edge- CSB Bank CreditFederal Card statements with actual outstanding, even after closure of the card account.

- In case the Edge- CSB Bank Credit Card has not been used for more than one year then we will notify the Cardholder of the dormancy within 30 days from the dormancy date. If the card is still not used or no reply is received for the continuation of Edge- CSB Bank Credit Card, Edge- CSB Bank Credit Card will be closed and reported to the bureau, subject to payment of all dues by the Cardholder.

Loss, theft or misuse of Card

Procedure to be followed in case of loss/theft/misuse of Edge CSB Bank Credit Card:-

- In case the Edge CSB Bank Credit Card is lost, stolen, misplaced, or if the credit card PIN has been compromised, report this immediately to customer support from the Jupiter app or via phone or email.

- If the Edge CSB Bank Credit Card is misplaced, the Cardholder can freeze the card temporarily from the Jupiter App.

- If the Edge CSB Bank Credit Card is lost or stolen, the cardholder can block the Edge CSB Bank Credit Card from the Jupiter app and place a request to reissue their card. The Cardholder can also reset the Edge CSB Bank Credit Card PIN from the Jupiter app. The Cardmember shall not be able to use the blocked Card for any transaction/s until the Cardmember receives a replacement Card.

- In case the mobile phone with the Jupiter App is lost or stolen, inform us immediately by calling +91 86550 55086. Please also report the theft of the Edge- CSB Bank Credit Card or phone to the police by lodging a First Information Report (FIR) and share a copy of that with us when requested.

- The Card Member shall not be liable for any transaction/s made on the Card post the Cardholder reporting the loss/theft/damage. However, in case of any dispute relating to the time of reporting such loss/ theft/damage and/or transactions made on the Card post reporting of the loss/theft/damage/ misuse, the Bank reserves the right to ascertain such time and or the authenticity of the disputed transactions.

Liability: Your liability in case of any of the above mentioned scenarios would be as follows:

- Zero liability where the unauthorized transactions occur in the following events:

- Contributory fraud/negligence/deficiency on part of the Bank

- Third Party breach where the deficiency lies elsewhere in the system and you notify the Bank (including its outsourced service providers) within 3 working days of receiving the communication from the Bank (or any of its outsourced service providers) regarding the unauthorized transaction.

- You shall be liable for the loss occurring due to unauthorized transactions in the following cases:

- In cases where the loss is due to your negligence such as where you have shared the payment credentials, you will bear the entire loss until you report the unauthorized transaction to the Bank (or any of its outsourced service providers). Any loss occurring after the reporting of the unauthorized transaction shall be borne by the Bank.

- In cases where the responsibility of the unauthorized electronic banking transaction lies neither with the Bank nor You, but lies elsewhere in the system and when there is a delay of 4-7 working days after receiving communication from the Bank (or any of its outsourced service providers) on your part in notifying the Bank of such a transaction, your per transaction liability shall be limited to the transaction value or the amount whichever is lower as mentioned in the table below (as per RBI)-

iii) Further, if the delay in reporting by You is beyond 7 working days, your liability shall be determined as per the Bank’s board approved policy.

Disclosures

- CSB Bank has tied up with Credit Information Companies (CICs) authorised by the RBI and will share credit information including but not limited to the current balance, loans / EMI facilities linked to Edge- CSB Bank Credit Card (if availed), balance outstanding on Edge CSB Bank Credit Card/ loan, payment history etc., along with the demographic details with these organisations on a monthly basis, as per the Credit Information Companies (Regulation) Act, 2005. The CICs only provide factual credit information and do not provide any opinion, indication or comment pertaining to whether credit should or should not be granted. It is in the best interest of the Cardholder to maintain a good credit history by paying the necessary dues in a timely manner. Details of default would also be available with the CICs, which in turn could impact your credit worthiness.

- CSB Bank reserves the right to report a delinquent customer to the CICs even in an instance of Cardholder raising a billing dispute which the Bank and/or its authorised service provider had clarified as an invalid dispute earlier or the dispute being raised by Cardholder after the cut-off date i.e. 30 days from the date of statement generation, and/or the dispute is in relation to secured transactions where a PIN or a One Time Password was used. The following steps will be followed in the reporting of delinquent customers to CICs

- Bank will report delinquent users to CICs within 15 days of the user turning delinquent

- You will be notified by SMS and email 7 days prior to being reported to CICs

- If you settle the required dues after being reported, Bank shall update the status within 30 days from the date of settlement of dues

- In case there is a dispute under investigation, you will be reported only after the settlement of the dispute, if required.

- CSB Bank Credit Bank and/or its authorised third party service providers will provide the particulars of the card account to the statutory authorities, as may be required. The Bank and/or its authorised by the Bank will share the necessary information including but not limited to that which is required for execution of the rewards programs, portfolio statistical analysis, etc., will be provided to Jupiter, in each case in accordance with applicable laws.

- You should also know that CSB Bank or its service provider , at its own discretion, records specific conversations between the Cardholder and any representative of the Bank, in cases of support or grievance-related conversations or payments-recovery-related conversations or any other conversations, that the Bank may deem fit.

- CSB Bank also reserves the right to assign any activities related to the credit card operations to any service provider appointed by the Bank, whether located in India or overseas and whether a Bank or a third party, at its sole discretion, in accordance with the applicable regulatory guidelines. CSB Bank can provide/share details of Cardholder application to such service providers for any activities related to the credit card operations without any specific consent. Bank or its authorised service provider authorised by the Bank the right to retain the application forms and documents provided therewith, including photographs, and will not return the same.

- From time to time CSB Bank and/or Jupiter authorised by the Bank communicates various products/features/promotional offers which offer significant benefits to its Cardholders and may use the services of third party agencies to do so. If the Cardholder does not wish to receive any direct marketing, SMS, Emails or telephone calls from the Bank for such services, the Cardholders may email us at support@jupiter.money. The Cardholders will continue to receive communication pertaining to the core features of the credit card.

- Edge CSB Bank Credit Card cannot be used for the purchase of prohibited items such as lottery tickets, banned or proscribed magazines, participation in sweepstakes, payment for call back services, and / or such items / activities for which no drawal of foreign exchange is permitted. Usage of the Edge CSB Bank Credit Card for transacting outside India must be made in accordance with applicable law, including the Exchange Control Regulations of the RBI and the Foreign Exchange Management Act, 1999, and in the event of any failure to do so, you may be liable for penal action.

- Foreign exchange trading through internet trading portals is not permitted. In the event of any violations or failure to comply, Cardholders may be liable for penal action and /or closure of card.

- Parties agree that any disputes in respect of any issues arising out of Terms and/or card usage, shall be referred to the non- exclusive jurisdiction of courts in Mumbai, India and shall be governed by and construed in accordance with the laws of India. The Cardholder further acknowledges that CSB Bank, Customer, shall appoint to refer the dispute to a sole arbitrator, in accordance with the provisions of the Arbitration and Conciliation Act, 1996 as may be amended, or its re-enactment. The arbitration proceeding shall be conducted in English language. The award passed by the arbitrator shall be final and binding on the parties. The arbitration proceedings shall be held at Mumbai or such other place as may be notified at the sole discretion of the Bank . The seat of arbitration shall be Mumbai. The Arbitration proceedings may also be held through video conference. To attend any hearing ordered by the tribunal, the following shall apply:

- Any such hearing shall be held via video conference upon the order of the tribunal;

- The parties agree that no objection shall be taken to the decision, order or award of the

- tribunal following any such hearing on the basis that the hearing was held by video conference.

- The Cardholder agrees that if at any time it is discovered that there are any amounts due to the Bank against any credit facility, then the Bank shall have the absolute right to hold the No objection certificate (NOC) against any/all such facilities, without any prior notice.

- Bank and its respective employees, agents or contractors shall not be liable for, and in respect of any loss or damage whether direct, indirect or consequential, including but not limited to the loss of revenue, profit, business, contracts, anticipated savings or goodwill, loss of use or value of any equipment including software, whether foreseeable or not, suffered by the user or any person, howsoever, arising from or relating to any delay, interruption, suspension, resolution or error of the Bank in receiving and processing the request and in formulating and returning responses or any failure, delay, interruption, suspension, restriction, or error in transmission of any information or message to and from the telecommunication equipment of the user and the network of any service provider and the Bank's system or any breakdown, interruption, suspension or failure of the telecommunication equipment of the user, the Bank's system or the network of any service provider and / or any third party who provides such services as is necessary to provide the facility.

J) Important Regulatory Information

- Your Edge CSB Bank Credit Card is valid for use both in India as well as abroad. It is, however, not valid for making foreign currency transactions in Nepal and Bhutan.

- Foreign exchange trading through Internet trading portals is not permitted. In the event of any violations or failure to comply, you may be liable for penal action and/or closure of the card.

- Outstanding dues may also be recovered from any of the operative accounts of the Cardholder maintained with the Bank as a part of the auto recovery process.

- Recovery of dues in case of death/permanent in capacitance of the Cardholder including insolvency and bankruptcy: It shall be in accordance with the applicable laws after giving sufficient notice for payment of dues and all information regarding the outstanding dues, to the successors/nominees /legal heirs/guardian of the Cardholder.